Sell in May: Does This Stock Market Adage Come into Play

“Sell in May and go away” is probably the most widely cited stock market cliché in history. Every year a barrage of Wall Street commentaries and stories in the financial press floods in about this popular, but overused, stock market adage. Here we take our annual look at this historical seasonal pattern which, as you will see below, has started to lose some of its street creds recently.

What is sell in may?

“Sell in May and go away” is the seasonal stock market pattern in which stocks generally produce the best returns from November through April and the worst returns from May through October. This pattern has been strong enough—and the adage popular enough—that it has probably been somewhat of a self-fulfilling prophecy over many years. Some investors do think it’s best to either avoid or reduce equities during this period. We’re not so sure.

The two figures below illustrate this pattern. Figure 1 shows average returns by calendar month (data back to 1950). Here you can see stocks tend not to do as well during middle months, on average, particularly May through September.

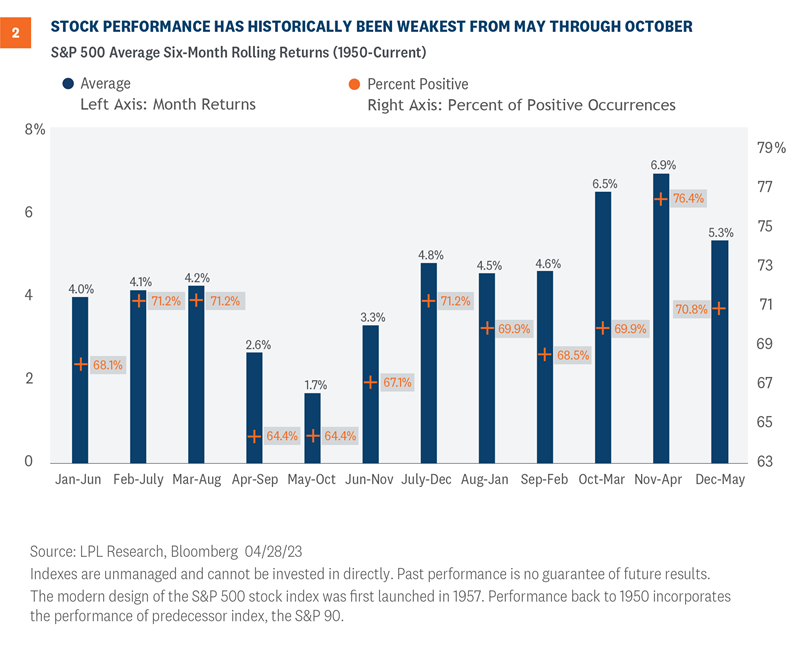

Figure 2 illustrates rolling six-month returns for each of the 12 rolling six-month periods by month (again, data back to 1950). Here you see the weakest six-month period for stocks historically, on average, has been May through October (1.7%), while the best six-month period has come between November and April (6.9%).

Interestingly, the S&P 500 was up 7.6% over the past six months (November through April), roughly in line with the historical average. That may suggest a typical gain for the next six months might be in order. That’s not great, but it’s not terrible. We think we can make a good case for an upside beyond that 1.7% between now and Halloween. And that would still leave the seasonally strong November and December months for the S&P 500 Index to reach our year-end fair value target range of 4,300–4,400.

In recent years, buy-in may has worked better

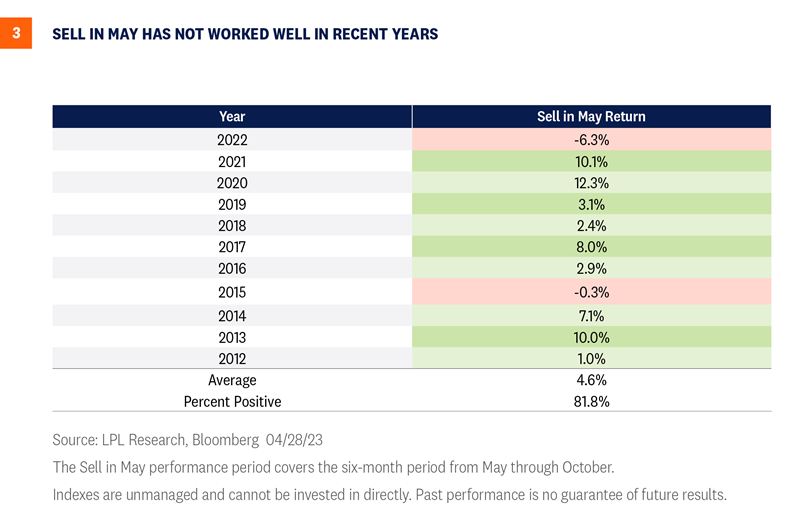

We should also keep in mind, as we head into this seasonally weak period, that the S&P 500 has closed higher during the month of May nine out of the past 10 years—so maybe the pattern should be “Sell in June.” Also, consider that this seasonally weak period has actually been quite strong in recent years. In fact, stocks gained during this seasonally weak six-month period in nine of the past 11 years, as you can see Figure 3.

So what about this year?

Our year-end fair value target for the S&P 500 implies about a 4% upside over the balance of 2023, That target is based on a price-to-earnings ratio (P/E) of 18 and our 2024 earnings forecast of $240 (though that estimate is under review, and the Strategic and Tactical Asset Allocation Committee’s (STAAC) bias is to potentially bring that estimate down some). The “right answer” to potentially get us there may actually be a higher P/E and lower earnings, though we’ve been encouraged by first-quarter earnings results thus far (more on that topic here in the coming weeks).

Assuming stocks generate another 4–5% upside between now and year-end, the question is when do those gains come? Gains late in the year would make sense because of this seasonal pattern and opportunities to 1) gain more clarity on the path of the economy and 2) make progress bringing inflation down to help get the Federal Reserve (Fed) off the market’s back.

On the other hand, market sentiment and traders’ positioning are pessimistic enough that maybe just bringing the Fed’s rate hiking campaign to an end this spring, getting past the debt limit increase, and seeing earnings avoid a collapse (which we’re clearly seeing during the current earnings season) could be enough to push this market higher. Finally, if the “Sell in May” pattern hasn’t worked well in recent years, maybe it won’t in 2023.

Our guess is more gains come later in the year, and that we see a 5–10% pullback between now and Halloween as is typical (we get three of those a year, on average), but that is not a high conviction prediction.

Investment Outlook

As stocks enter a seasonally weak period with near-term macro risks ahead, investors may not want to stray too far from their benchmark exposures to equities. Stocks are getting more support from earnings than we had anticipated, but earnings declines aren’t over. While the May rate hike from the Fed may be its last of this cycle—we’ll learn more about that when we hear from Fed Chair Jerome Powell and company on Wednesday—clearly the inflation problem hasn’t yet been solved.

Bottom line, LPL Research remains comfortable with its year-end S&P 500 fair value target of 4,300–4,400. But as stocks get closer to that target, LPL Research’s Strategic and Tactical Asset Allocation Committee (STAAC) may reconsider its recommended slight overweight allocation to equities. The Committee notes that the outlook for growth stocks has improved, suggesting balanced style exposure, while the outlook for small caps has gotten more challenging in recent weeks, as credit conditions have tightened amid ongoing small bank stress. The industrials sector remains the Committee’s top pick.

Within fixed income, the Committee recommends an up-in-quality approach with a benchmark weight to duration. We think core bond sectors (U.S. Treasuries, Agency mortgage-backed securities, (MBS) and short-maturity investment grade corporates) are currently more attractive than plus sectors (high-yield bonds and non-U.S. sectors) with the exception of preferred securities, which look attractive after having recently sold off due to the banking stresses.

Jeffrey Buchbinder, CFA, Chief Equity Strategist

Adam Turnquist, CMT, Chief Technical Strategist