Q4 Earnings Preview: Pessimism May Be Overdone

Fourth quarter earnings season is underway and probably won’t bring much good news. Lackluster global growth, ongoing profit margin pressures from inflation, and negative currency impacts are likely to translate into a year-over-year decline in S&P 500 Index earnings for the quarter. As always, guidance matters more as market participants look forward. The key question coming into this earnings season is whether the pessimism surrounding 2023 earnings has gone too far.

A number of headwinds

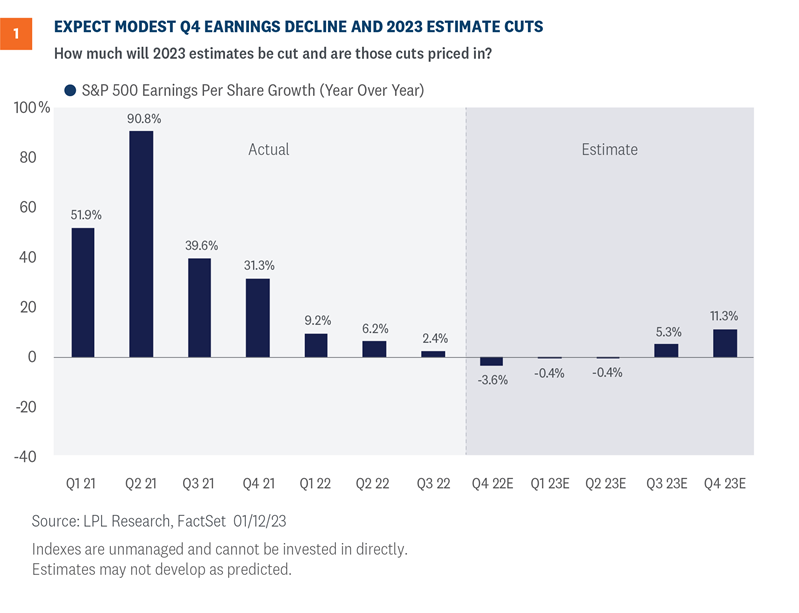

As was the case last quarter, corporate America faces several stiff headwinds this earnings season. These headwinds—clearly not new news—include slower global economic growth, cost pressures from still-elevated inflation, ongoing supply chain issues, currency drag from a stronger U.S. dollar last quarter compared with the year-ago quarter, and geopolitical instability, particularly in Eastern Europe and China. These headwinds will likely translate into a slight year-over-year (YOY) earnings decline for the S&P 500 in the fourth quarter, with an outside shot at getting above the flat line (Figure 1).Consensus currently stands at -3.6% YOY in the quarter (source: FactSet).

The good news is some of these pressures have started to abate, particularly currency pressures, after a 9% drop in the U.S. dollar since the fourth quarter began on October 1 (though it was up about 6% YOY in Q4). Even the economic pressures have eased some, with fourth quarter U.S. gross domestic product (GDP) likely to exceed the 1.2% consensus forecast of economists surveyed by Bloomberg based on the latest data. And don’t forget the U.S. economy grew at a solid 3.2% pace in the third quarter of 2022, while Europe has held up better than we anticipated, thanks in large part to falling natural gas prices.

Bottom line, if we’re going to get enough upside for the S&P 500 to grow earnings at all in Q4, it will likely come from the resilience of the U.S. and European economies, currency effects, and some mitigation of profit margin pressures from cost controls and lower inflation.

Guidance is key

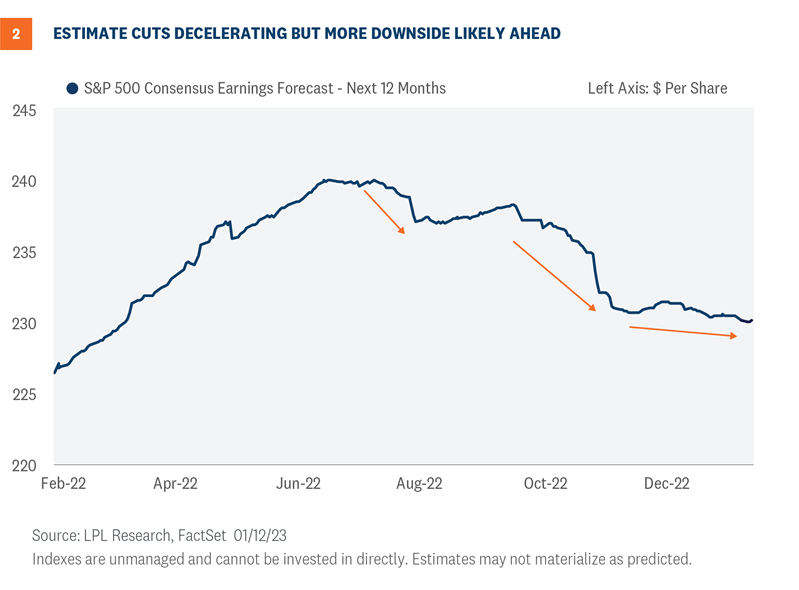

The key question to answer this earnings season is whether the pessimism surrounding 2023 earnings has gone too far. LPL Research believes that it probably has. Admittedly, analysts have been too slow to bring S&P 500 earnings estimates for 2023 down from the current $230 per share level to a more reasonable $215 to $220 range (our estimate is currently $220, flat or down slightly from 2022 levels). A mild recession would likely take us down to $210 or lower, depending on how fast and how much inflation comes down later this year.

As shown in Figure 2, estimates have come down substantially over the past two quarters, but the pace of cuts has slowed heading into fourth quarter earnings season. That may indicate estimates may not have to come down 10%-plus in the near term as some market strategists expect.

Here are some reasons why estimate cuts may not be as drastic as some fear:

- China’s reopening—uneven or not—is well underway and may be a catalyst for supply chain fixes and more global demand.

- Companies have had plenty of time to prepare. If a recession occurs this year, it may be the most anticipated recession in history.

- Cost pressures have started to ease, taking some of the pressure off margins. Examples include lower energy prices and slowing wage increases.

- Recession may be a more than 50/50 proposition, but it isn’t inevitable. The U.S. economy may “muddle through” and skirt recession.

- Revenue growth is solid, bolstered by the higher revenue that comes with inflation. Consensus is calling for a 3.8% YOY increase in fourth quarter S&P 500 revenue, but recent quarterly trends suggest a 5% increase is possible.

Pushing in the other direction is the 1–2% hit to S&P 500 earnings expected this year as a result of the tax increases in the Inflation Reduction Act (which, as we’ve shared in the past, won’t do much to lower inflation this year). Soft manufacturing activity and ongoing inventory adjustments in certain segments of the economy, such as semiconductors, will also be a drag on earnings in the near term.

Bottom line, we would look for 2023 earnings estimates to come down, but not collapse, this reporting season. The path to a sub-$220 number for S&P 500 EPS estimates this year, if we get there, will be gradual. Modest cuts in the coming weeks may actually be a positive catalyst for stock prices.

Pay attention to earnings season, revisions matter

With so much disagreement about the 2023 earnings outlook, maybe it’s not a tough sell to convince investors that earnings matter. We often hear analysts projecting the seemingly obvious “earnings matter” refrain; of course earnings and fundamentals matter, but at times of irrational exuberance—though not as much in 2022 and 2021—and meme stocks (see here), we feel the need to yell it even louder. Beyond the obvious reasons to pay attention during earnings season, there are quantitative trading trends that support paying attention to earnings, and more importantly, forward estimate revisions.

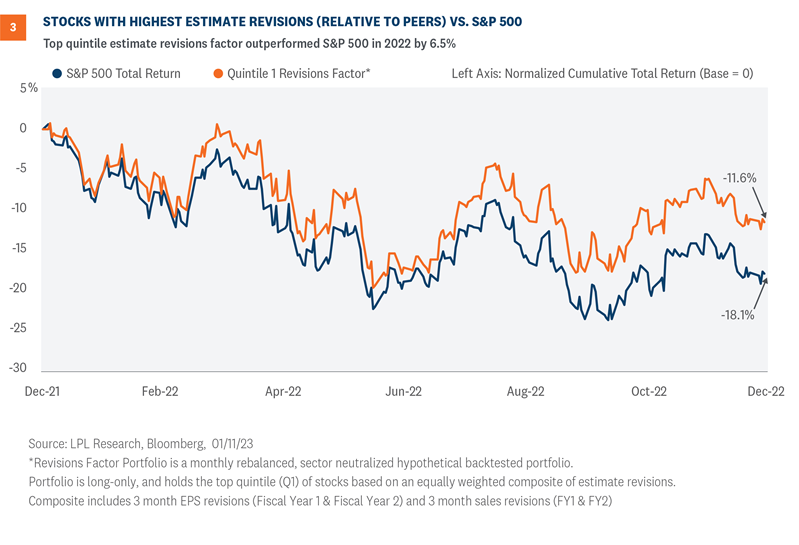

LPL Research’s quantitative research team created a revisions composite factor, which combines four estimate revisions metrics (current and following fiscal year EPS and sales estimate revisions over last three months) into one standardized score.

Using the S&P 500 as the investible universe, a hypothetical long-only portfolio is constructed of the top quintile (top 20 percent) of stocks’ estimate revisions composite score. This portfolio is equally weighted and rebalanced monthly. Looking at 2022 in isolation, this strategy would have outperformed by about 6.5% to 7%, depending on whether you neutralize sector effects or not.

Figure 3 shows the hypothetical performance of the sector-neutralized portfolio vs. the S&P 500 on a total return basis. We analyzed this phenomenon by sector, and while most sectors showed positive performance vs. their cap-weighted sector index, there were sectors that underperformed. This estimate revision phenomenon provides a compelling backdrop for fundamental stock picking and provides another tool for investors to use in equity and sector selection.

Conclusion

This earnings season likely won’t offer much in the way of good news. We saw that in the challenges the banks faced in their reports on Friday, January 13 (an inauspicious date to start earnings season). But pessimism may be overdone, and investors may be surprised at how well stocks hold up on the news. Look for earnings throughout the next year to exceed those pessimistic forecasts and—along with falling inflation and the end of Federal Reserve rate hikes—serve as positive catalysts for solid gains for stocks in 2023.

Jeffrey Buchbinder, CFA, Chief Equity Strategist, LPL Financial

Thomas Shipp, CFA, Quantitative Equity Analyst