Earnings Preview – Malaise Continues

First quarter earnings season kicks off this week with some big banks reporting toward the end of the week. In some ways this quarter’s earnings season will probably be déjà vu all over again—earnings declines and cautious guidance, reductions in estimates, but better than feared. However, tightened financial conditions in the wake of last month’s banking turmoil and building evidence for a slowing economy have changed the economic backdrop this quarter. It will be interesting to see how management teams react to these latest developments.

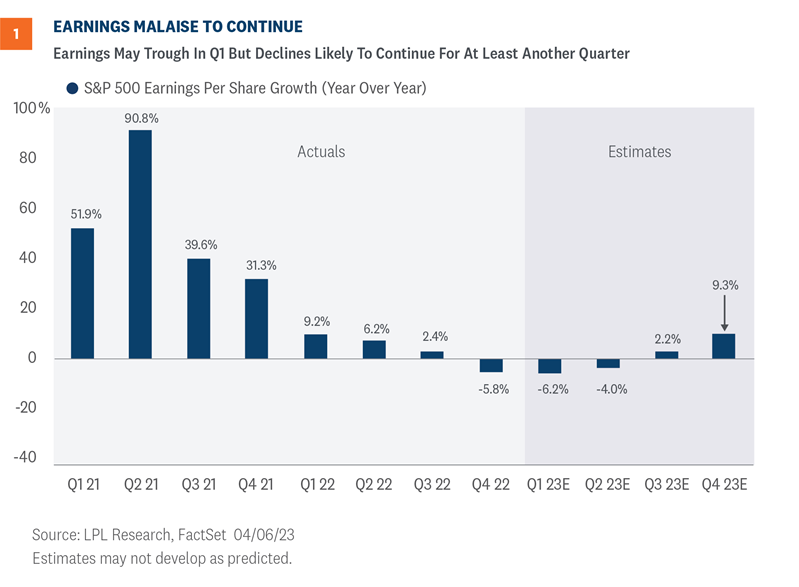

Setting the stage

Corporate America faces some of the same headwinds it did during fourth-quarter earnings season, including slow global economic growth, cost pressures from still-elevated (but easing) inflation, some currency drag from a stronger U.S. dollar last quarter compared with the year-ago quarter, and geopolitical instability, particularly in Eastern Europe and China, that has put some upward pressure on costs. Add bank stress that will weigh on financial sector profits and we have the makings of another year-over-year (YOY) earnings decline for the S&P 500 Index in the first quarter. Any upside to the current consensus estimate for S&P 500 EPS at -6.2% YOY (source: Factset) will be difficult to achieve, (Figure 1), and a second straight quarterly miss—even if rare—may be in the cards.

It’s not all bad news though. Inflation pressures have continued to abate, potentially helping to mitigate pressure on profit margins. The labor market has loosened a bit, limiting wage increases. The U.S. dollar has come down about 10% since October 2022, which helps earnings from U.S.-based multinational companies. And while calls for recession have become commonplace, the U.S. economy very likely grew in the first quarter—consensus first-quarter gross domestic product (GDP) growth tracked by Bloomberg is 1.3%. Meanwhile, Europe’s economy continues to hold up better than most anticipated and will probably not be much of a drag.

Finally, the bar for this earnings season has been lowered quite a bit, with first-quarter estimates cut by 6% during the quarter, about double the long-term average.

Earnings and the economy are closely tied

The weakness in the Institute for Supply Management (ISM) manufacturing and services indexes is a reason to expect earnings declines and weak guidance this quarter. Looking at services specifically, released on April 5, the index fell to 51.2 from 55.1, down from over 58 a year ago. This reading implies a weakening outlook for both businesses and consumers.

In Figure 2 we show the relationship between the ISM Services Index and S&P 500 operating earnings growth. Services is a much larger piece of the U.S. economy than manufacturing, but given corporate America is more manufacturing-oriented, the relationship with the manufacturing ISM, or the composite (manufacturing plus services) looks virtually identical.

The components of the ISM surveys provided further evidence of a slowing economy, including a 10-point drop month over month in services new orders. As the economy slows and inflation decelerates, the Federal Reserve (Fed) will be in a better position to pause the current rate hiking campaign, although that will likely be accompanied by weak earnings in the first half of this year, and potentially beyond.

Margin guidance will be the key

During fourth-quarter earnings season, a number of companies were rewarded for cost-cutting measures, particularly in the technology sector. For this upcoming earnings season, expect more of the same. Analysts will be sharpening their pencils when it comes to costs. Revenue will hold up fine—remember, the inflation we pay is more revenue for someone else.

Layoffs were initially constrained to tech names, where excessive hiring took place during the pandemic. However, recent announcements have spread to companies in other sectors, and the market’s response to more recent cost-cutting news has been mixed (McDonald’s and GM are examples). While layoffs help control costs and improve margins, they can also weigh on consumer spending and eventually translate into less business investment. On this score, the gradual pace of the labor market loosening, rather than a sharp reversal, has been positive. We hope to see wage pressures ease because of fewer openings rather than layoffs, which we saw this week in the Job Openings and Labor Turnover Survey (JOLTS).

We seemingly say it every quarter, but in this uncertain environment, guidance matters more than actual results. And specifically, cost/margin guidance is key.

Uncertainty reigns for the rest of the year

In two decades closely following strategists’ forecasts for S&P 500 EPS, it’s hard to recall a time when there was more disagreement about the path of profits. This is when looking at different scenarios can be helpful.

- In a muddle-through economic scenario, we would expect S&P 500 earnings to hold up fairly well and potentially hit current consensus estimates of around $220.

- In a mild, short-lived recession, perhaps $210 is a reasonable forecast.

- In a typical recession that perhaps lasts a year, we would expect something closer to $200 per share in 2023 EPS, or about a 10% year-over-year decline.

If we probability weight these, with a slightly higher probability for muddling through (perhaps (50%), 35% odds for a short-lived, mild recession, and a 15% chance for a typical recession, we end up with a number in the $213–$215 range.

For now, we’ll keep our $220 forecast in place for 2023, but we would consider that number under review until we hear from corporate America. Our 2024 S&P 500 EPS number will almost certainly come down, but lower interest rates support higher stock valuations, so we think stocks will get to the same place by year-end. The 10-year Treasury yield, near 3.4%, was about 0.8% higher five weeks ago.

Investment Outlook

Stocks may not get much support from earnings in the near term as the malaise continues. However, we do expect the market to benefit from the end of the Fed’s rate hiking campaign—likely in May. Higher interest rates may challenge stock valuations this year, but we still see the potential for additional gains for stocks over the next nine months.

LPL Research remains comfortable with its year-end S&P 500 fair value target of 4,300–4,400. While that target was set based on a price-to-earnings ratio (P/E) of 18 and a 2024 EPS estimate of $240, the P/E may be a bit higher and the earnings number a bit lower when all the results are in.

The LPL Research Strategic and Tactical Asset Allocation Committee (STAAC) recommends a slight overweight allocation to equities, narrowly favors value over growth, has moved to benchmark-level exposure for small and large caps, has the industrials sector as its top pick, and has warmed up to the technology sector, where the overall view is currently neutral, but the technical analysis picture has improved significantly this year.

Within fixed income, the Committee recommends an up-in-quality approach with a benchmark weight to duration. We think core bond sectors (U.S. Treasuries, Agency mortgage-backed securities (MBS), and short-maturity investment grade corporates) are currently more attractive than plus sectors (high-yield bonds and non-U.S. sectors) with the exception of preferred securities, which look attractive after having recently sold off due to the banking stresses.

Jeffrey Buchbinder, CFA, Chief Equity Strategist